As we grow and transition through each chapter of our lives, our priorities and goals change — on everything from sleeping habits to major life decisions.

The same is true when it comes to financial well-being and growing wealth. Where you are on your journey will likely guide your feelings around spending, saving, investment strategies, and broad financial goals.

But when it comes to growing wealth, there are several basic essential principles to follow, no matter where you are in life: Spend less than you make, stick to a spending plan, and invest for the future you want.

Here’s a look at how different life stages may impact your financial goals in the short- and long-term.

The accumulation phase: Working hard for your money

This stage begins when you start your career and continues through the majority of your working years.

Financial priorities – Short-term goals and debt management

During this phase, your financial priorities will likely be various shorter-term goals, such as saving for a new car, a wedding, your first home — or all three (and then some). Your success during this time often hinges on how you balance reaching these goals with managing debt and savings.

While not all debt is bad, it’s critical to your financial progress that it remains manageable. When used strategically to help you fund major goals, such as buying a house or perhaps a new business, debt can help you get there a bit quicker. You simply want to consider how your debt payments work with your overall spending and savings plans.

Of course, the more debt you have, the less you are able to save. And your savings will be the key to all your other short- and long-term goals.

Investment outlook – Save and invest for long-term goals

Time is one of the most valuable things you have on your side during this phase. That means it’s worthwhile to prioritize longer-term financial goals, such as saving for retirement or even a child’s education. The sooner you begin investing for longer-term goals, the more your money will be able to grow, thanks to the beauty of compounding.

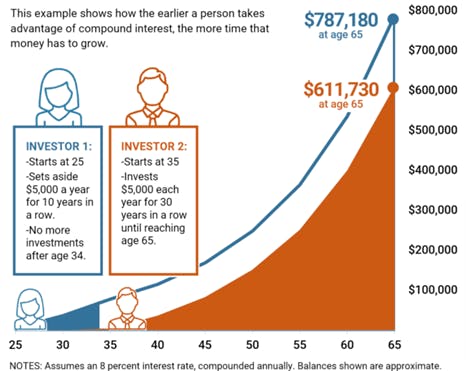

The chart below shows just how much a longer time frame can benefit your investments’ ability to grow.

Source: Federal Reserve Bank of St. Louis1

As you can see, the investor who started saving earlier in life had a larger balance by retirement — even when stopping contributions after 10 years.

Of course, if you were to continue investing all through your working years, your retirement balance would have the opportunity to grow even greater.

The pre-retirement phase: Preparing for a major transition

As you near the end of your career, it’s time to start thinking about your transition into post-work life. This phase usually begins when you are within 10 years of retirement.

Financial priorities – Determine your needs in retirement and manage expenses

At this point in life, it’s time to quantify the different elements of your retirement plan, such as how much you need to retire comfortably and what your retirement spending might look like.

To do this effectively, visualize the life you want in retirement. For example, do you plan to move? Do you see yourself taking frequent trips? Would you like to make a major purchase, like a boat or RV?

This part is critical, but it can also be fun and motivating as you begin to imagine and look forward to the next phase of your life.

Hopefully, you’ve done a good job of managing your expenses up to this point and haven’t accumulated too much debt. If you do have any outstanding debt, you may want to prioritize paying it off as much as possible before you retire. A debt-free retirement can be less stressful because you’ll have greater flexibility with your spending.

Investment outlook – Adjust existing strategies and “catch up” if necessary

If you already have a long-term retirement plan in place, your investment approach may not have to change too much. However, this is an important time to review your progress and confirm you’re still on track. Also, ensure your investments still match your risk tolerance and align with your timeline and goals.

Because the later years of your career could be your peak earning years, you might be able to double down on progress. Making extra debt payments or taking advantage of retirement “catch-up” contributions are both excellent ways to do this.

The retirement and distribution phase: Enjoying your hard work

If you prepared accordingly throughout your previous stages in life, then this should be the point when you relax and enjoy what you’ve worked so hard to accomplish over the years.

Financial priorities – Reconcile your relationship with money and optimize tax expenses

Once you retire, you’ll move from building wealth to spending it. But how you go about that will depend entirely on your goals.

At this point, you’ll want to consider what your money really means to you. Your outlook will also influence your budget and withdrawal strategy.

For instance, consider the following questions:

- What does your money need to do for you?

- Are you enjoying your wealth, or are you too afraid to spend it?

- Do you plan to use all your savings, or would you prefer to give some away?

It’s incredibly important that you understand your expenses in retirement. This is the primary factor that determines how long your money will last.

Tax management should also be a central consideration of your withdrawal strategy. The right tactics can save you significant money — often adding years to your portfolio longevity. For example, you may wish to consider strategies, such as Roth conversions, to help you decrease your tax burden on withdrawals.

Investment outlook – Manage for risks and market volatility

Retirement isn’t the time to forget about your investments. In fact, for retirees, one of the most dangerous risks to your savings could be a significant dip in the market during the early years of retirement.

If the market declines significantly, it can be challenging to recover without the right plan in place. Just as a financial advisor can help you navigate saving before retirement, they can also help you manage risk and determine a distribution strategy in retirement.

Statistically — with a little luck — you are likely to live as a retiree for several decades, so your money still needs to work for you.

No matter where you are in life, we can help you reach your goals

Financial planning is a crucial task during each stage of your life. Of course, the particular focus will vary over time to adjust to your changing circumstances. But a well-thought-out financial plan can help ensure those changes are productive and ultimately help you fulfill your life’s goals.

To learn more or get in touch with a financial advisor that can help you with your plan, reach out to our team today.

The commentary on this website reflects the personal opinions, viewpoints, and analyses of the Trinity Wealth Management, LLC employees providing such comments, and should not be regarded as a description of advisory services provided by Trinity Wealth Management, LLC or performance returns of any Trinity Wealth Management, LLC Investments client. The views reflected in the commentary are subject to change at any time without notice. Nothing on this website constitutes investment advice, performance data, or any recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Trinity Wealth Management, LLC manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

Sources:

1 “How Does Compound Interest Work?” Federal Reserve Bank of St. Louis