A Mid-Year Economic Outlook: Are Better Times Ahead or Will Inflation and the Bear Market Persist?

September 15, 2022

Economic headlines in 2022 have been notably tumultuous: the highest levels of inflation in 40 years, a contracting economy, and a market downturn. Yet, amid the worrisome news, investors may still find plenty of reasons to be optimistic.

With more than half of the year already behind us, here’s our economic half-time report about what’s happened so far, what might be ahead, and what investors should keep their eyes on for the rest of the year.

A Tale of Two Economies

The past two years seem to tell the stories of two very different U.S. economies. As the country emerged from the pandemic lockdowns, 2021 proved to be a banner year. The nation’s gross domestic product (GDP) for the entire year increased by a robust 6.3% after taking inflation into account.

Four key tailwinds in 2021 propelled that strong growth, including the following:

- Economic stimulus from both the Trump and Biden administrations pumped $5 trillion into the economy, helping keep individuals and businesses solvent throughout the pandemic.

- The Federal Reserve (Fed) kept interest rates near zero and returned to its bond purchasing program, known as “quantitative easing.” Both measures supported the economy by increasing the money supply and keeping the financial system liquid. In total, the Fed increased the money supply by 40% during the pandemic.

- The development and distribution of vaccines helped slow the spread of COVID-19 and enabled the reopening of the economy.

- Geopolitics remained relatively stable. Russia was massing troops along the Ukrainian border, but there was hope leadership might not take further action.

All these factors helped stage a strong turnaround for the economy, as it quickly put the severe slowdown brought on by the early days of the pandemic in the rearview mirror.

Tailwinds Converted to Headwinds in 2022

Initial expectations were that 2022 could bring a continuation of 2021’s trends. However, the economy, as measured by GDP, contracted by 1.6% in the first quarter. Many of the conditions that supported strong growth in 2021 shifted from tailwinds to headwinds.

- The government’s fiscal stimulus program ended, although government checks left consumers flush with cash they wanted to spend.

- The Fed began to taper its quantitative easing program, and high inflation forced the U.S. central bank to raise interest rates at relatively high increments of 50 and 75 basis points (0.50% and 0.75%). At the end of 2021, the Fed’s federal funds target rate was near zero. As of its last meeting in July 2022, the Fed brought its benchmark rate from 2.25% to 2.50%, with its fourth increase of the year. With further hikes, the rate is expected to be 3.25% to 3.50% at year-end.

- New COVID-19 variants, like Omicron, caused China to lock down 45 cities, impacting 400 million people. The lockdowns, which lasted for months in some areas, prevented people from going to work, which brought further disruptions to global supply chains.

- Russia ultimately invaded Ukraine, bringing geopolitical turmoil and disrupting global food and energy markets.

The economic setback raised the specter of recession, which is generally defined as two consecutive calendar quarters of negative economic growth. This definition appears to have been met, given that the U.S. economy, according to the latest revision to GDP numbers, contracted by 0.6% in the second quarter.1 Yet, many economists debate whether the economy is truly in a recession because so many economic conditions, like consumer spending and employment levels, have been strong.

Still, the consolation from some positive economic indicators has been offset by one major challenge: inflation.

Why Has Inflation Been So High?

A basic rule of economics is prices are determined by supply and demand. They shift whenever there is an imbalance between the two. When supply exceeds demand, prices tend to come down. When demand outpaces supply, prices go up. The latter scenario is what’s playing out in 2022.

Still flush with cash from the fiscal stimulus, consumers have been eager to spend. The Fed’s steps to increase the money supply also mean more dollars are in the system to support spending.

However, with global supply chain disruptions, companies haven’t been able to maintain the inventory levels necessary to meet the greater demand. A vicious cycle has also ensued: Consumers worried about inflation are attempting to buy more because they anticipate prices on the goods and services they want will soon be higher. What economists call “inflation psychology” has taken hold.

Russia’s invasion of Ukraine exacerbated the inflation problem because it disrupted global energy supply chains and caused oil and gas prices to spike. With inflation high, many consumers wonder if soaring prices constitute a weak economy and a recessionary environment. The answer, as many economists agree, seems to be “no.”

Jeffrey Frankel, a professor of capital formation and growth at Harvard, explained to Barron’s in June that “inflation isn’t recession, which is defined as a significant decline in economic activity. Economic activity is not falling. Quite the contrary: It is booming.”2

Even though the nation’s GDP decreased in the first quarter and was modestly down in the second quarter, other economic indicators remain quite strong.3 The unemployment rate was 3.7% in August, a slight uptick but still low and reflective of a strong economy. The U.S. labor market added 315,000 jobs in August.4 That represented the 20th consecutive month of job growth, a trend that continues to propel the economy amid high inflation.

So, if certain segments of the economy have been so strong, it’s natural to ask why the GDP numbers for 2022 have been weak.

The answer comes when examining the four sectors that contribute to GDP. As Exhibit 1 illustrates, consumer spending, government spending, and business investment all increased in the first quarter. The one contributor to GDP that declined was net exports. Other countries didn’t recover from the pandemic-induced slowdown as quickly as the United States. Therefore, the volume of goods U.S. consumers purchased from other markets far outweighed the level of goods U.S. companies sold to consumers in other countries. The lack of demand from foreign consumers caused the U.S. economy to contract in the first quarter.

EXHIBIT 1: DECLINE IN NET EXPORTS CONTRIBUTED TO U.S. GDP DECLINE IN Q1

Changes in the four components of GDP during Q1 2022

What’s Next?

With the unusual combination of high inflation and strong underpinnings for the economy, many are debating what’s to come. There appear to be three possible scenarios:

- Soft landing: This could occur if the Fed’s pace of interest rate increases proves to be effective enough to tame inflation without negatively impacting economic growth, thereby avoiding recession.

- Stagflation: This would be the unwelcome prospect of high inflation with a stagnant economy. So far, this seems to be the less likely scenario given that many economic factors, like job growth, have remained strong even with high inflation.

- Recession: This scenario could result if the Fed — through its efforts to combat inflation — is so aggressive with rate hikes that it slows the economy. A true recession could begin if the country’s GDP declines even further, employment weakens, and consumer spending declines.

Luckily, experts appear to be optimistic that a soft landing could occur while they offer cautionary notes. For example, Brian Swint, acting deputy bureau chief of Barron’s, said in July, “A lot of damage has been done by high energy prices. But if they fall back soon, as history suggests they should, the second half of 2022 could be much better than most people currently expect.”5 (In the weeks following this published quote, energy prices did begin to fall, as evidenced by lower prices at the pump.)

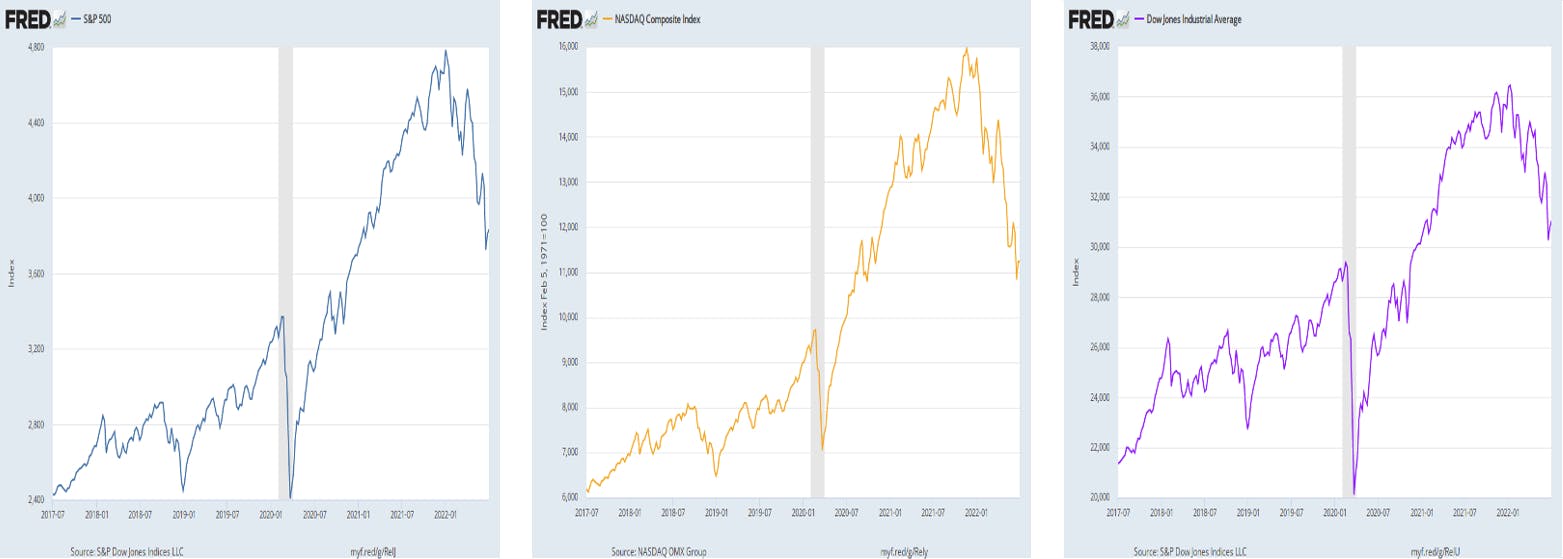

Are We in a Bear Market? If So, How Long Will It Last?

A bear market is defined as a sustained period when stocks remain 20% below their levels reached during a previous peak. For the first half of the year, the S&P 500 was down 21%.6 Three major U.S. stock indexes — the Dow Jones Industrials Average, Nasdaq Composite, and S&P 500 — all experienced significant losses, as illustrated in Exhibit 2. The market’s performance from January to June of 2022 represented the worst half year for stocks in 50 years.

EXHIBIT 2: WORST HALF YEAR FOR STOCKS IN IN 50 YEARS7

Most sectors experienced significant declines, but some posted gains. Healthcare and consumer staples saw modest increases, while utility stocks posted average price gains of 10.66%. Energy stocks, fueled by higher oil and gas prices, soared by an average of 35.85%.

Collectively, companies’ earnings, which are usually a reliable indicator of the long-term direction of stock prices, have been strong. Further hikes in interest rates may trim earnings a bit, but the current overall expectation for earnings growth for the year is 10.2%.8

However, recent stock performance suggests markets are quite concerned about the Fed’s commitment to being aggressive with rate hikes, as Fed Chair Jerome Powell signaled it would be during a talk at the Fed’s Jackson Hole Symposium in late August.

What’s an Investor to Do?

During severe market downturns, investors may want to exit the game and remain on the sidelines until the turmoil ends. They might consider shifting from stocks to cash and then hope they can reenter the market once the upturn begins.

But trying to time the market rarely works. It’s extremely difficult to predict when the rebounds will come, and they often do in short, sudden bursts. Being out of the market and missing the best recovery days can greatly hinder your returns.

A better alternative might be to apply the time-tested principles of long-term investing. These include:

1. Stay invested when pursuing long-term goals.

For goals more than 10 years away, the market’s short-term gyrations are not likely to have a major impact on your returns. History has shown bear markets eventually recover, and stocks have a good track record of delivering solid long-term returns for investors. Your behavior could impact your returns more than the market’s short-term volatility.

2. Let your goals, risk tolerance, and time horizon drive your strategy.

To manage risk, you can allocate your holdings across a variety of assets and diversify within each asset class. Your goals, risk tolerance, and time horizon should determine how aggressive or conservative you’ll want to be.

3. Work with a professional advisor.

A financial advisor can help you identify investments appropriate for your goals and choose asset allocation and diversification strategies that match your risk temperament. An advisor can also remove emotions from investing and provide an objective outlook when you have concerns about the market’s performance. An advisor may even help you seek the opportunities down markets may bring. For instance, you could use the short-term declines as buying opportunities to invest in companies with good long-term prospects whose stock prices may be temporarily available at a discount.

Keep Events in Perspective

There is no question the first half of 2022 was difficult for both the stock market and the U.S. economy in terms of GDP growth numbers and inflation. Now, the question is whether the market downturn and economic slowdown will continue, and how long they might last if they do.

No one has a crystal ball, but the good news is the economy is showing some signs of strength. Most economists are not making dire predictions for what lies in the months and quarters ahead. However, investors can take solace in knowing that history suggests the markets and economy eventually recover, and those who stay calm in the midst of difficult times typically fare better.

Learn more about how the economy could affect your portfolio and the steps to consider by speaking with a Trinity Wealth Management financial advisor. Our team is prepared to assist clients as they navigate financial planning and investment management during volatile and unpredictable markets. Get started with us today!

The commentary on this website reflects the personal opinions, viewpoints, and analyses of the Trinity Wealth Management, LLC employees providing such comments, and should not be regarded as a description of advisory services provided by Trinity Wealth Management, LLC or performance returns of any Trinity Wealth Management, LLC Investments client. The views reflected in the commentary are subject to change at any time without notice. Nothing on this website constitutes investment advice, performance data, or any recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Trinity Wealth Management, LLC manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

Sources:

1 “Second-quarter GDP declined less than previously thought, but the economy is still shrinking,” CNN Business

2 “Inflation Isn’t Recession. The Chances of a Downturn Are Lower Than People Think.” Barron’s

3 “Charting the Global Economy: Unemployment Rate in US Climbs,” Bloomberg

4 “Labor market added 315,000 jobs in August: A bright spot in the economy,” The Washington Post

5 “Oil Falls Below $100. Prices Could Drop Even Further,” Barron’s

6 “S&P 500 had worst first half in 50 years, but the 60/40 portfolio isn’t dead,” CNBC.com

7 “S&P Dow Jones Indices LLC,” FRED, Federal Reserve Bank of St. Louis

8 “Earnings Insight, 2022,” FactSet Research Systems