A Mid-Year Outlook: Have We Weathered the Storm?

September 1, 2023

As 2023 began, the markets braced for recession. Many market observers were sure that the Federal Reserve’s battle to contain inflation—with 10 rate hikes in 14 months—would tip the U.S. economy into a slowdown.

Yet, remarkably, the slump never arrived. Unemployment remained low, ending the first half at 3.6%. Wage growth accelerated. By the end of the first half, job creation had slowed somewhat, but U.S. consumers were working and earning enough to feel good about spending. Even adjusted for inflation, personal spending hit a new high in June.1

There was also good news on the inflation front, as the Fed’s aggressive policy took effect. CPI was up just 4% in May, year-over-year, after peaking in June 2022 at 9.1%. Of course, the job isn’t finished yet. The Fed may raise rates again in 2023 as it works towards its target of 2% inflation. But with growth continuing and inflation receding, the question has increasingly become, can the U.S. Economy stick the soft landing the Fed is hoping for?

The Case for a Soft Landing

When the Fed raises rates to combat inflation, it can cause one of two scenarios, a soft or hard landing. In a soft landing, economic growth slows as the Fed raises rates, but there is no recession. In fact, after an initial decline, economic growth may be steady or pick up.

In a hard landing, by contrast, rising rates cause the economy to contract, triggering a recession, and with it, often job losses and market volatility. The Fed then has to reduce rates in order to try to bring the economy back to health.

Right now, we are seeing increasing signs of a soft landing. Inflation is down, even though prices remain high compared to recent years. Unemployment rates are low, but new job growth is starting to slow. Wages are growing strongly, and consumer spending remains robust, despite higher prices and higher costs of borrowing due to high interest rates.

Consumer spending has propped up the U.S. economy to such a degree that many market observers now believe that the Fed can tame inflation without a recession. More than two-thirds of business economists surveyed in August said that they thought the Fed would achieve a soft landing, up from just 30% in March.2

A Rally in Stocks But Trouble in the Bond Markets

Financial markets rallied as the threat of recession receded. The Standard & Poor’s 500 Index entered a bull market in June, rising 20 percent from its October 2022 low. There may be more ahead, too, since historically, stocks have performed well after a 20 percent gain. In fact, the S&P 500 has added to its initial 20 percent jump in 12 out of 13 bull markets since 1956, with an average additional gain of 17.7% over the next year.

AI continues to be a driver for solid performance from technology stocks, as the market recognizes the productivity-enhancing potential of large language models and other machine learning technologies. Industry leaders in AI, including Nvidia, Apple, Amazon, Alphabet, Meta Platforms, Microsoft, and Tesla, accounted for much of early 2023’s strong market gains.3 Information technology led all other sectors in the first half of 2023 with a 42.06% advance.

Earnings were down 2% in the first quarter of 2023, but have, for the most part, beat expectations. Seventy-eight percent of S&P 500 companies reported better-than-expected earnings per share for the first quarter, while eight of 11 sectors saw year-over-year revenue growth.

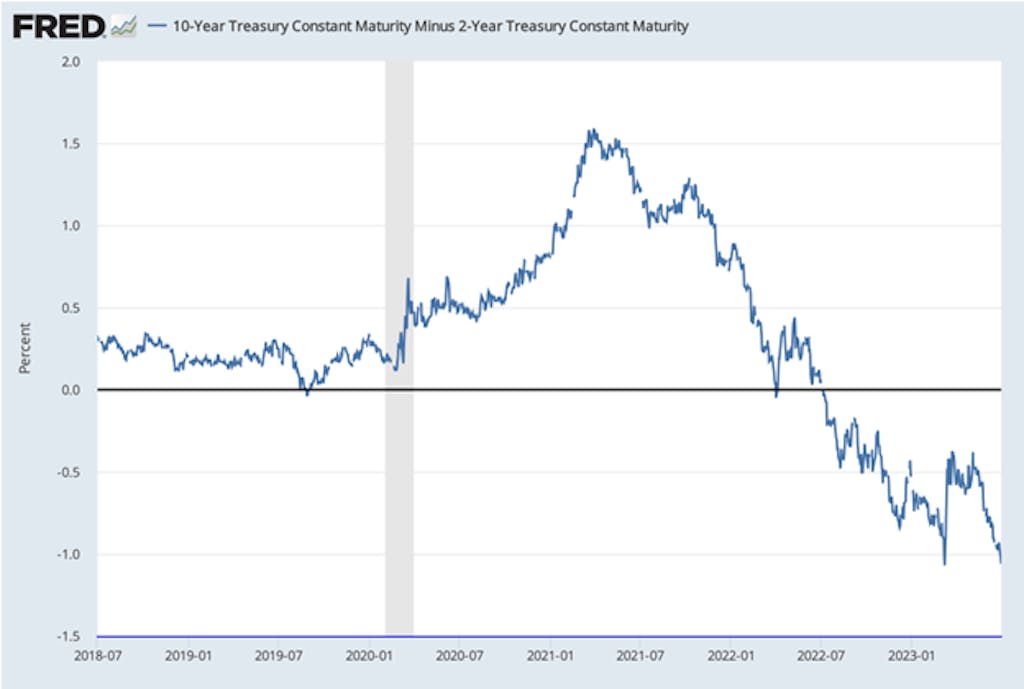

The bond markets have had a challenging year, which is not unusual when rates rise. However, one feature of the fixed-income markets in 2023 was atypical: an inverted yield curve.

Normally investors expect higher yields when they lend their money for longer periods. That is, you will receive a higher interest payment on a 10-year bond than a 2-year bond. However, for most of this year, shorter-maturity Treasuries have yielded more than longer-maturity Treasuries.

The chart above shows the difference in yield between 2-year U.S. Treasuries and 10-year U.S. Treasuries. As you can see, we entered negative territory in July 2022 and have remained there ever since.

Why is this important? Often yield inversions foreshadow recessions. However, the Cleveland Federal Reserve cautioned that, while “yield curves contain important information for business cycle analysis” it has not always been an accurate predictor.

Expectations for Growth in 2024

Growth may be slower in 2024 if we enter what economists call “stagflation.” This is an environment in which inflation remains high even as economic growth lags. In this scenario, the Fed would likely continue to raise interest rates for as long as it takes to control inflation. The process can be painful, as higher rates for longer periods often lead to job losses, negative investor sentiment, and financial market turmoil.

Against this negative backdrop, however, we do see some positive signs. AI and technology continue to drive growth and innovation. Indeed, one study by McKinsey estimated that generative AI could add between $2.6 and $4.4 trillion to the global economy.4 That’s about as much as a mid-sized country. Moreover, AI is not the only transformative technology under development. Advances in areas like longevity, digital smell, super apps, and virtual power plants all have the potential to create significant market value in the years to come.

We remain concerned about high levels of debt in the U.S., as the government deficit has increased to a staggering $31.4 trillion. However, inflation and economic growth have whittled away at this number in real terms. The debt-to-GDP ratio fell from a peak of 135 percent in mid-2020 to 120 percent at the end of 2022 —mostly because GDP increased by $4.4 trillion over that period. In addition, inflation of 12 percent in 2021 and 7 percent in 2022 has cut into the real value of the deficit.

What matters most, of course, is whether the government can pay its debt, and here, the signs are encouraging. Tax receipts are up sharply as employment rises, more than outstripping the additional costs of higher interest payments.

Surprising Economic Strength and Signs of a Soft Landing

Earlier in the year, many economists were certain that we would be hit by a major recession by this point, but it has yet to materialize. Inflation and rising interest rates have continued to put pressure on the spending power of the American consumer, but solid employment numbers and rapidly rising wages have helped to offset those challenges.

We may not be out of the woods just yet, but the general picture of the U.S. economy has solidified over the past several months, and a “soft landing” may yet be on its way.

Learn more about how the economy could affect your portfolio and the steps to consider by speaking with a Trinity Wealth Management financial advisor. Our team is prepared to assist clients as they navigate financial planning and investment management during volatile and unpredictable markets. Get started with us today!

The commentary on this website reflects the personal opinions, viewpoints, and analyses of the Trinity Wealth Management, LLC employees providing such comments, and should not be regarded as a description of advisory services provided by Trinity Wealth Management, LLC or performance returns of any Trinity Wealth Management, LLC Investments client. The views reflected in the commentary are subject to change at any time without notice. Nothing on this website constitutes investment advice, performance data, or any recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Trinity Wealth Management, LLC manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

Sources:

- “Personal Income and Outlays,” Bureau of Economic Analysis, June 2023. https://www.bea.gov/news/2023/personal-income-and-outlays-june-2023#:~:text=Definitions,in%20the%20form%20of%20transfers

- “More Analysts Believe Economy Will Have A ‘Soft Landing’” Investopedia, August 21, 2023. https://www.investopedia.com/more-business-leaders-believe-economy-will-have-a-soft-landing-7724616

- “The US stock market just had its best year — so far — since 1997,” CNN, August 1, 2023. https://www.cnn.com/2023/08/01/business/stock-market-best-performance-july/index.html

- “The economic potential of generative AI: The next productivity frontier,” McKinsey, July 2023. https://www.mckinsey.com/capabilities/mckinsey-digital/our-insights/the-economic-potential-of-generative-ai-the-next-productivity-frontier#introduction