Today, 45 million borrowers have a cumulative $1.6 trillion1 in federal student loan debt — the second-largest type of debt held by U.S. consumers.

In an effort to help ease the burden for those with substantial college loan debt, U.S. President Joe Biden announced a Student Loan Relief Plan in August 2022.

The plan promises to help up to 43 million eligible college and graduate school borrowers, including the cancellation of all outstanding student loan balances for up to 20 million of these borrowers.

While the plan is intended to provide relief for those with debt and burdensome monthly payments, one considerable result is how taxpayers and long-term education costs will be affected.

So, let’s take a closer look at the relief plan, along with its potential benefits and consequences.

How the Student Loan Relief Plan Works and Who Is Eligible

The Student Loan Relief Plan is comprised of the following four key components3:

Outright Debt Cancellation

The Department of Education will cancel up to $20,000 in debt for federal Pell Grants recipients and up to $10,000 for those who didn’t receive these grants. To be eligible for this relief, individuals must have annual earnings of less than $125,000 while families must have annual earnings of less than $250,000.

Extension of Student Loan Forbearance

At the outset of the pandemic, the government suspended required loan payments4 and collections on defaults while also introducing a temporary 0% interest rate on most federally held student loans. That forbearance has now been extended until December 31, 2022.

New Rules for the Income-Driven Repayment (IDR) Plan

The Education Department is changing the IDR plan so federal student loan borrowers will not have to pay more than 5% of their monthly income in loan payments. The previous limit was 10%. This change could reduce the average borrower’s loan payments by as much as $1,000 annually.

The amount borrowers are expected to repay is based on their discretionary income. And the new IDR rules will raise the amount of income considered non-discretionary. Borrowers with annual earnings below 225% of the federal poverty level will not have to make monthly payments. This is more generous than the previous threshold of 150%.

For those who had original loans of less than $12,000, their loan balances will now be forgiven after 10 years of payments, rather than 20 years under the old rule. The Department of Education estimates this change will eliminate outstanding loan amounts after 10 years for all borrowers who attended community colleges.

Borrowers’ unpaid monthly interest will be covered, as well. This change will ensure a borrower’s outstanding balance can’t grow even during periods when their monthly required payment is zero because their current income is low.

It’s important to keep in mind that under IDR plans, any debt that is forgiven becomes taxable income in the year of forgiveness. The new proposed rules do not address this, so borrowers may end up with a large future tax bill. You may wish to speak with a tax professional to determine how this might impact your tax liability.

Adjustments to the Public Service Loan Forgiveness (PSLF) Program

The Education Department is revising this program, which provides debt cancellation for people who worked for 10 years in public service jobs for federal, state, local, or tribal governments or nonprofit organizations.

One of the changes includes offering debt cancellation or credits toward debt forgiveness5 for those who have worked for such organizations for less than 10 years, but the deadline for applying for this relief is October 31, 2022.

How the Bill May Provide Relief for Borrowers

College students now graduate with an average of almost $30,000 in debt.6

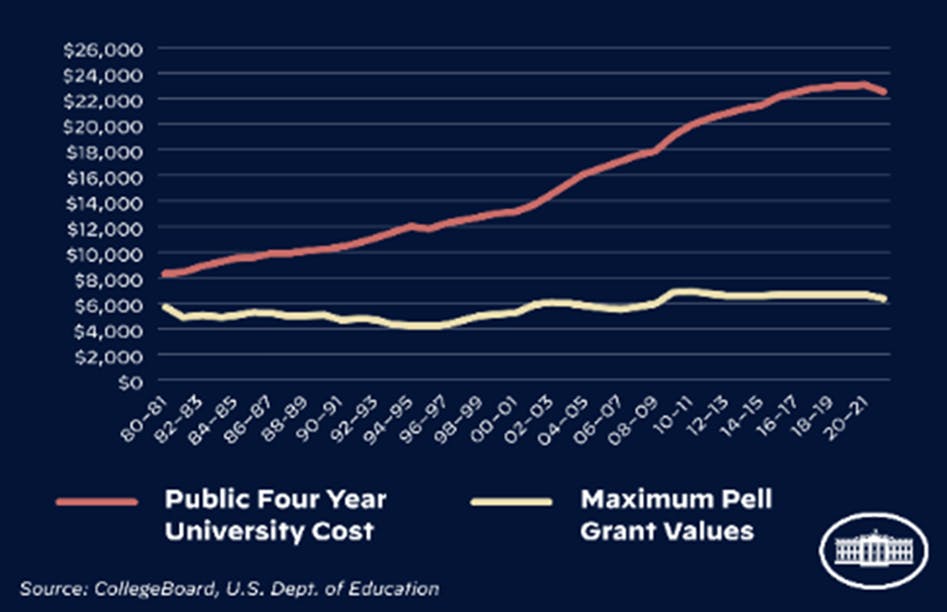

In recent decades, low- and middle-income families had few options to receive loan-free aid to cover the high cost of college. And sources of free financial aid, like the federal Pell Grants, have not increased at rates close to the degree at which college costs have soared (see Exhibit 1).

Exhibit 1: Sources of Free Financial Aid Haven’t Kept Pace with College Costs

All the changes to the federal student loan program will make managing this debt less burdensome. Now, many borrowers will be able to make substantially lower monthly payments, and others will have all their remaining debt canceled.

Federal student loans are not forgivable, even in bankruptcy proceedings. So, these changes will provide more ways for those overwhelmed by their outstanding debt to make their student loan payments manageable.

Borrowers will have to act quickly to take advantage of this relief. Some of the initial deadlines for applying for assistance take place in fall 2022. Borrowers can sign up for alerts about the relief program at www.ed.gov/subscriptions.

Who’s Footing the Bill for the Student Loan Relief Plan?

Providing this much relief to student loan borrowers will cost the federal government a pretty penny.

The Wharton School of the University of Pennsylvania estimates that the total cost of the program could be $605 billion, with the potential to reach $1 trillion.8

Its initial estimates project that:

- The proposed student loan debt cancellation will cost between $469 billion and $519 billion over 10 years.

- The loan forbearance granted in 2022 could cost an additional $16 billion.

- Changes in the income-driven repayment (IDR) plan could cost an extra $70 billion. Depending on the plan changes and how borrowers respond to them, these changes could add $450 billion to the cost of the relief plan, thereby bringing its total cost past the $1 trillion mark.

Taxpayers will have to pay for those federal expenditures. Using the Penn Wharton Budget Model, the National Taxpayers Union Foundation projected9 what one portion of the student loan relief program, the cancellation of $10,000 in debt for borrowers making less than $125,000 per year, might cost individual taxpayers.

This change, which might cost a total of $329.1 billion over 10 years, could translate into a significant increase in the tax obligations of high-income earners especially, as outlined in Exhibit 2.

Exhibit 2: Impact of the Student Loan Relief Program on Taxpayers10

| Income Level | Potential Cost per Taxpayer Due to Debt Cancellation |

| $1-$50,000 | $158.27 |

| $50,000-$75,000 | $866.87 |

| $75,000-$100,000 | $1,477.78 |

| $100,000-$200,000 | $3,158.35 |

| $200,000-$500,000 | $9,947.92 |

| Average for all taxpayers | $2,085.89 |

Of course, these are just preliminary estimates. The actual cost of these policies will not be known for some time.

How the Relief Plan Could Increase Long-Term College Costs

While the student loan relief plan appears to decrease the education burden on a per-student basis, it could negatively affect long-term college costs.

These changes could establish a major disconnect between the nominal and actual costs of college. Estimates project the changes could mean borrowers who take out federal student loans would have to pay only 50 cents for every dollar they borrow.11 This knowledge might intrigue students to take out more debt than they would if they were on the hook for the entire loan. That scenario could cause the collective level of student loan debt to balloon again.

Any circumstances that make students less concerned about the expense of borrowing could also provide incentives for colleges to raise their costs even more exorbitantly. This appears to mirror a precedent set by law schools in a similar scenario.

Loan repayment assistance programs similar to the proposed changes in the IDR may make students less concerned12 about how much they must borrow to pay for law school. These graduate schools, perhaps in response to this reduced concern, have raised their tuition. The cost of legal education has increased more than 90% since 2005, with the average annual tuition cost rising from $29,417 to a projected $56,49613 for the 2021 to 2022 school year.

With the new broader student loan relief plan, a similar scenario could play out with schools offering undergraduate education and graduate programs in other disciplines.

We Can Help You Manage Education Costs

While the Student Loan Relief Plan helps many student loan borrowers, it may not solve the problem of rising education costs, and it potentially shifts the forgiven debt to taxpayers. The right financial advisor can help you plan for education, just like any other major expense or investment. Integrating these expenses into your overall financial plan is crucial, as is exploring ways to manage education costs, such as creating a 529 savings plan, evaluating the cost of borrowing, or considering lower-cost options like community college.

The advisors at Trinity Wealth Management can provide expert guidance on how to address your education savings needs. Contact us today to learn more about how we can help.

The commentary on this website reflects the personal opinions, viewpoints, and analyses of the Trinity Wealth Management, LLC employees providing such comments, and should not be regarded as a description of advisory services provided by Trinity Wealth Management, LLC or performance returns of any Trinity Wealth Management, LLC Investments client. The views reflected in the commentary are subject to change at any time without notice. Nothing on this website constitutes investment advice, performance data, or any recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Trinity Wealth Management, LLC manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

Sources:

1 “FACT SHEET: President Biden Announces Student Loan Relief for Borrowers Who Need It Most,” whitehouse.gov

2 “Consumer Debt Continued to Grow in 2021 Amid Economic Uncertainty,” Experian

3 “FACT SHEET: President Biden Announces Student Loan Relief for Borrowers Who Need It Most,” whitehouse.gov

4 “Student Loan Forbearance Extension: Can You Get It Extended?” SoFi

5 “Public Service Loan Forgiveness,” whithouse.gov

6 “See How Average Student Loan Debt Has Changed,” U.S. News & World Report

7 “FACT SHEET: President Biden Announces Student Loan Relief for Borrowers Who Need It Most,” whitehouse.gov”

8 “The Biden Student Loan Forgiveness Plan: Budgetary Costs And Distributional Impact,” Penn Wharton University of Pennsylvania

9 “Cost of Student Debt Cancelation Could Average $2,000 Per Taxpayer,” National Taxpayers Union Foundation

10 “Cost of Student Debt Cancelation Could Average $2,000 Per Taxpayer,” National Taxpayers Union Foundation

11 “Biden’s Income-Driven Repayment plan would turn student loans into untargeted grants,” Brookings Institution

12 “There’s a giant loophole in Biden’s student-debt relief that could make college even more expensive. Here’s how it works,” Fortune

13 “Average Cost of Law School,” Education Data Initiative