As you approach age 65 or begin planning for retirement, understanding your healthcare options becomes increasingly important. Medicare is a crucial part of that equation, but it can be confusing to navigate the different parts and plans available. The two most common choices are Original Medicare and Medicare Advantage.

While both options provide coverage for essential health services, they function quite differently. Here’s a breakdown of the key similarities and differences to help you understand which may align best with your personal needs.

What Is Original Medicare?

Original Medicare is the traditional program run by the federal government and is made up of:

- Part A (Hospital Insurance): Covers inpatient hospital stays, skilled nursing facility care, hospice, and some home health care.

- Part B (Medical Insurance): Covers outpatient care, doctor visits, preventive services, and medical supplies.

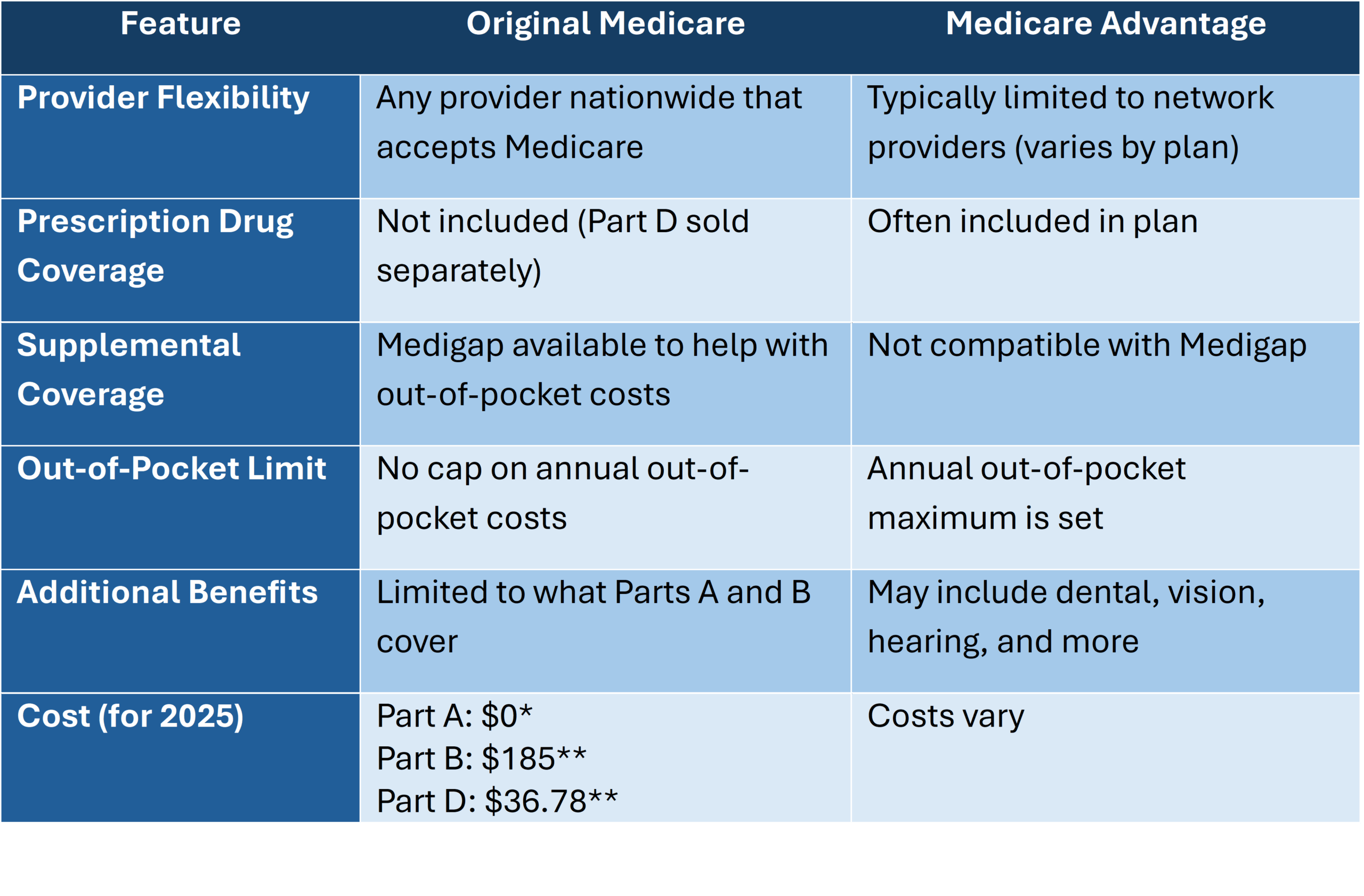

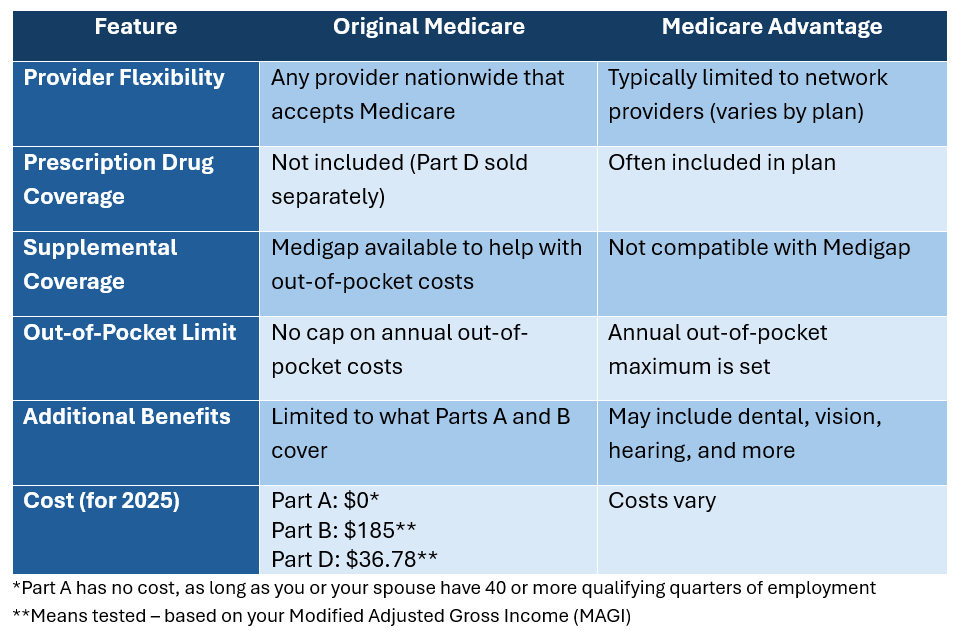

With Original Medicare, you can visit any doctor or hospital that accepts Medicare, nationwide. Most people pay a premium for Part B, and there may be deductibles, coinsurance, and out-of-pocket costs.

Because Original Medicare does not include prescription drug coverage, many people add a separate Part D plan to cover medications. You can also purchase a Medigap (Medicare Supplement Insurance) policy to help cover costs like copays and deductibles.

What Is Medicare Advantage?

Medicare Advantage, also known as Part C, is offered through private insurance companies approved by Medicare. These plans must provide at least the same coverage as Original Medicare (Parts A and B), but many go further, often including:

- Prescription drug coverage (Part D)

- Vision, hearing, and dental benefits

- Wellness programs or fitness memberships

Most Medicare Advantage plans use a network of providers, such as an HMO or PPO. This means you may need to stay within the plan’s network to receive full benefits, and referrals may be required for specialists.

Key Similarities

- Eligibility: You are eligible for Medicare at age 65, or earlier if you have certain disabilities or conditions. To join either Original Medicare or a Medicare Advantage plan, you must be enrolled in both Part A and Part B.

- Regulated by Medicare: Both are overseen by the Centers for Medicare & Medicaid Services (CMS), ensuring certain standards of coverage and consumer protections.

- Annual Enrollment Periods: Both plans have specific windows each year when you can enroll, make changes, or switch between options.

Key Differences

Things to Consider

Choosing between Original Medicare and Medicare Advantage depends on several factors:

- Do you travel frequently or want the flexibility to see any doctor?

- Are you looking for an all-in-one plan with additional benefits?

- Is having an out-of-pocket limit important to you?

- Do you prefer the predictability of a network plan or the freedom of nationwide coverage?

Choosing between Original Medicare and Medicare Advantage depends on your priorities, including flexibility, cost, and coverage. Both options offer important benefits, and the right choice is based on your individual situation.

If you are nearing Medicare eligibility or supporting a loved one through the decision, we are here to help.

Contact us to schedule a conversation. We would be happy to guide you through your options.

___________________________________________________________________________________

The commentary on this website reflects the personal opinions, viewpoints, and analyses of the Trinity Wealth Management, LLC employees providing such comments, and should not be regarded as a description of advisory services provided by Trinity Wealth Management, LLC or performance returns of any Trinity Wealth Management, LLC Investments client. The views reflected in the commentary are subject to change at any time without notice. Nothing on this website constitutes investment advice, performance data, or any recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Trinity Wealth Management, LLC manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.