Many investors and advisors have heard the old adage “Sell in May and Go Away,” a piece of investor wisdom based on the fact that historically, markets have performed better between the months of November to April, and worse from May to October. But is buying in May and “going away” really a sound investment strategy?

These ebbs and flows in the markets over periods of time are commonly called “market seasonality.”

Many investors have sought to create a strategy to leverage market seasonality to their benefit. However, this approach exposes investors to the reality that markets are, and always have been, a little unpredictable. So is it really worth trying to time the markets?

First, let’s look at how “selling in May” has fared for investors over time.

The Historical Performance of ‘Sell in May and Go Away’

When looking at an investment strategy, consider the historical precedent in both positive and negative markets. History does in fact show significant differences in performance from the months of November to April when compared with May to October.

Notably, nearly all of the major market downturns or crashes have come between May and October, including Black Monday, the DotCom Bubble crash, and most recently, the 2008 market crash.

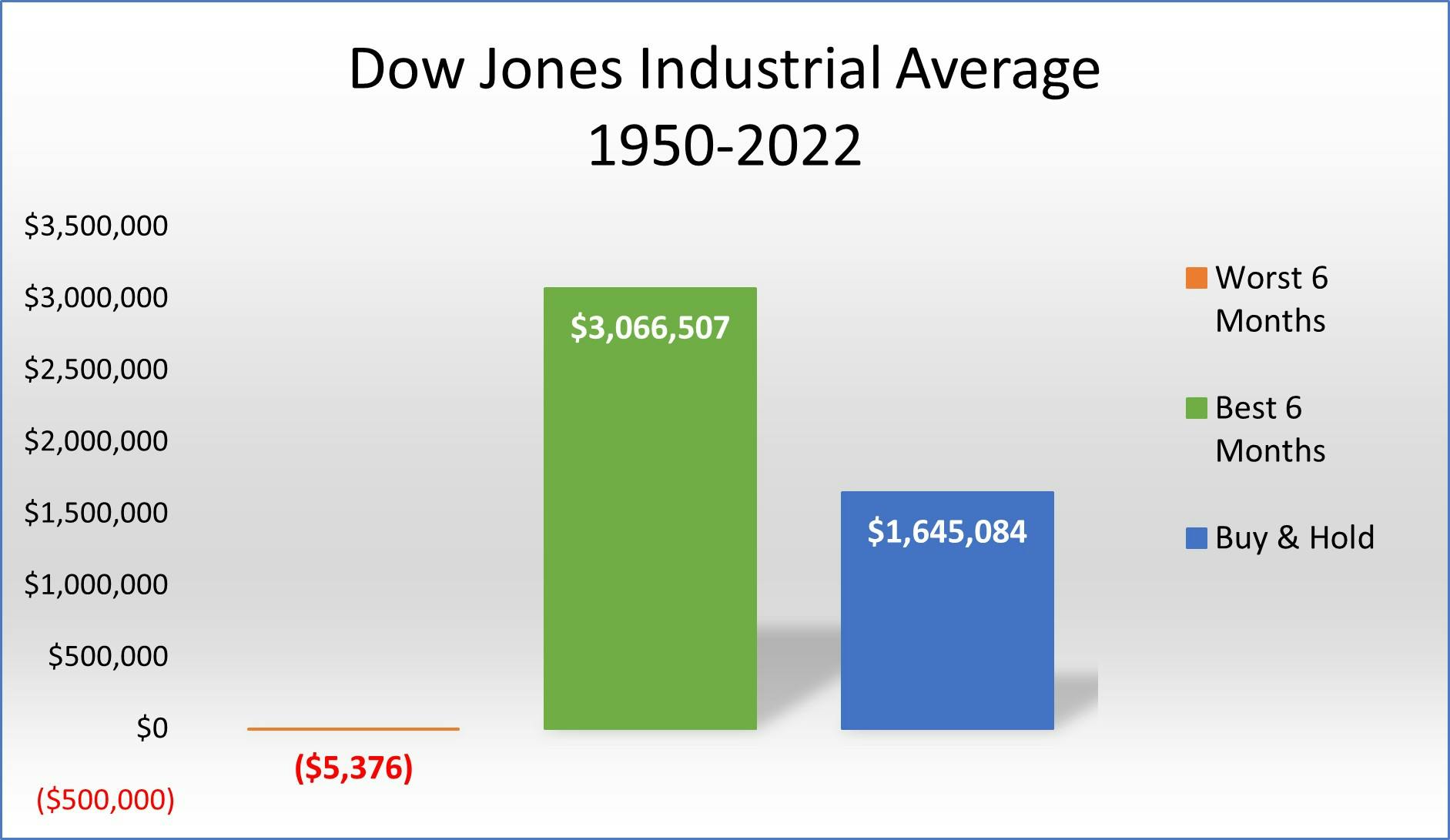

Based on research from the Stock Trader’s Almanac, an investment of $10,000 in the Dow Jones Industrial Average from 1950 through 2022 would have produced very different results depending on which months of the year you invested, as shown in the chart below:

If you only invested during the Worst 6 Months (May – October), your $10,000 investment would be worth a paltry $5,376. However, if you invested during the Best 6 Months (November – April), your $10,000 investment would have grown to $3,066,507. During these 72 years, the Best 6 Months even outperformed buying and holding the Dow Jones Industrial Average the whole time.

The challenge for investors though, is to assess the historical context that couples the performance. While there is evidence supporting the sell in May strategy on the surface, market factors always change over time, and it is important to not fall into complacency, or the assumption that what has worked in the past will work again in the future.

While all those major crashes did occur in the May-October period, they all also came as a result of much broader, and less predictable environments.

The concept of timing the markets remains a nearly impossible task. There are many strategies that attempt to capture potential gains and avoid potential losses, but markets are unpredictable, and these strategies don’t always achieve their goals.

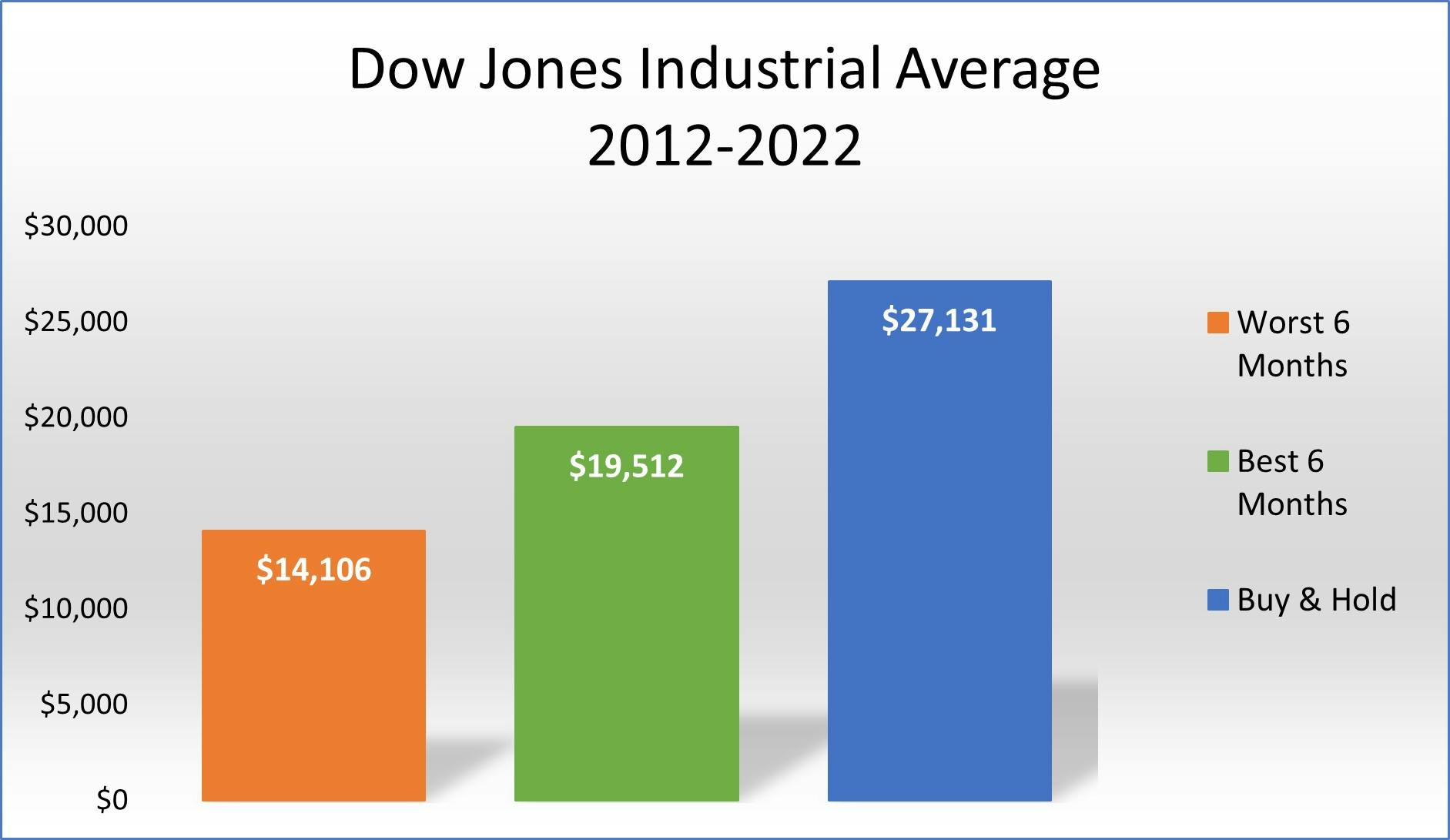

Let’s look at the last 10 years. While the Best 6 Months did perform better than the Worst 6 Months from 2012 through 2022, both time periods underperformed buying and holding the Dow Jones Industrial Average. The chart below illustrates an initial investment of $10,000:

What Would Have Happened if You Sold in May 2020?

Recent years have given us many examples that highlight the challenges of timing the market. In late-Spring 2020, for example, the COVID 19 pandemic caused severe disruptions to the historical trends we’ve been discussing. As the world went into lockdown, markets were dealt a serious blow, during what would typically be one of the “best” months.

In the months that followed, as lockdowns were slowly lifted and some “normalcy” came back to day-to-day life, markets experienced a significant comeback. In fact, from May to November of that year (worst 6 months), the S&P 500 gained 24.5% – compared to 17.8% during the best 6 months (November 2020 – April 2021).

We can hope, for many reasons, that the disruptions caused by the COVID 19 pandemic were outliers to the norm, but they do serve to illustrate how unpredictable events can throw a wrench in even the most time-tested strategies.

So what can investors really do to keep their portfolios secure, and growing throughout these cycles?

Staying the Course with an Effective Long-Term Strategy

While there will always be cyclical trends to consider in your portfolio construction, focusing on the long-term strategy over short-term factors is key. Relying on market seasonality and reacting to external events may help or hurt you in the short term, but ultimately, a long-term strategy focused on core fundamentals and objectives is more likely to deliver results that work for you.

Seeking the guidance of a financial professional can help align your investment goals with a portfolio strategy that works through all market environments. This can also help avoid cyclical thinking and set your portfolio up for long-term, sustainable success.

If you have questions about building your portfolio with your long-term goals in mind, or simply want to discuss how market cycles and external factors are impacting you, please feel free to contact the team at Trinity Wealth Management.

The commentary on this website reflects the personal opinions, viewpoints, and analyses of the Trinity Wealth Management, LLC employees providing such comments, and should not be regarded as a description of advisory services provided by Trinity Wealth Management, LLC or performance returns of any Trinity Wealth Management, LLC Investments client. The views reflected in the commentary are subject to change at any time without notice. Nothing on this website constitutes investment advice, performance data, or any recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Trinity Wealth Management, LLC manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.