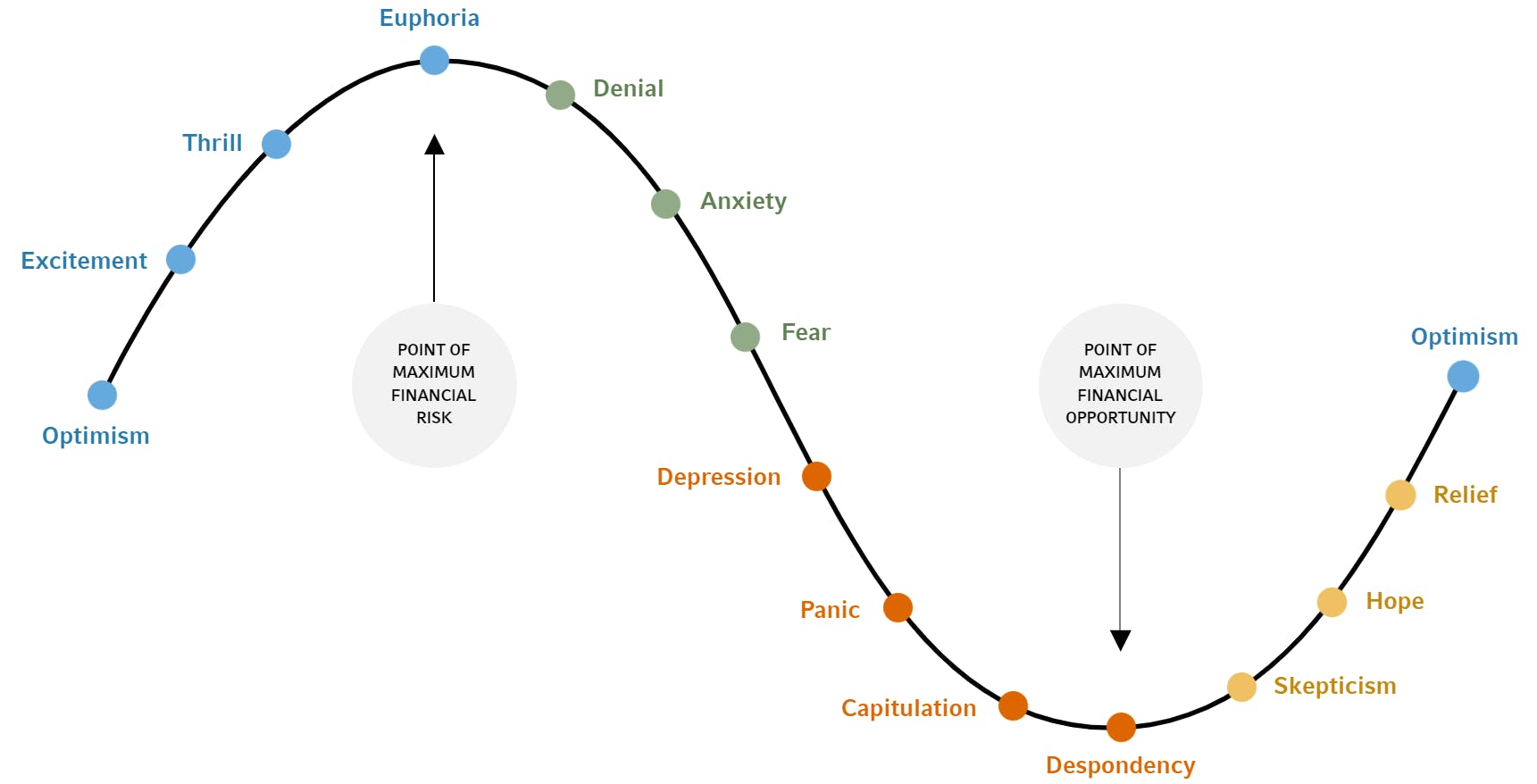

Just like stock market cycles, investors often cycle through a roller coaster of emotions when it comes to investing.

Optimism drives people to take more risk when the market is doing well, and fear makes them want to sell when the market is at the bottom.

While these are natural behavioral responses to market volatility, investors may want to avoid jumping on the bandwagon of reactionary market behavior. Doing so almost always leads to worse performance.

People may be drawn to certain investments because they like a company’s products or services (e.g., clothing, makeup, exercise equipment, software, car). But they may also find it hard to be objective about cutting ties to such investments when it makes financial sense to do so.

This same attachment applies when investors hold shares of their own employer’s stock. Owning employer shares may often reflect one’s loyalty to a company or pride in the products and services offered.

To avoid getting too emotional about your investments, here are some strategies to help you become a more rational and disciplined investor.

Set Limits

Knowing exactly how much downside you are willing to tolerate, and how much return you expect from an investment can allow you to implement a better investment plan. An effective exercise for helping you figure this out is measuring your risk tolerance. This will help you understand what you expect from your investments and allow you to match your choices with your goals.

- When you’ve reached your return objectives, you’ll have a predetermined point at which you know it’s time to trim your position and reinvest the gains elsewhere.

- If you reach your loss capacity, then you’ll know it’s time to sell and move on.

You can exercise an automatic limit for when to get in or out of an investment by using what’s known as a stop order. This is a type of order that you can place to limit your loss on an investment. Rather than a market order which executes immediately, a stop order is entered and remains in place until a triggering price is reached.

Suppose you buy shares of a stock for $80. You could set a stop-loss to sell the shares if the price falls to $72. You would set this order in advance – likely at the time you purchase the shares. If the stock price falls to $72, the shares are sold.

To effectively implement this strategy, you must decide what your limit is before you invest. In this example, that means you have decided that “If the share price hits $72, then I’m out”. Stop orders can also be placed to capture gains. For example, you may also place a stop order at $90 for your $80 shares.

By deciding beforehand, you can make a better decision because you have a clear mind that isn’t caught up in the fear or excitement of the moment. Once you make your decision it’s important to stick with it.

- Don’t cancel your stop order.

- Don’t immediately buy the stocks back.

Remember why you set the stop order in the first place.

Be objective; Hope isn’t an investment strategy

Avoid becoming attached to your investments. Your investments exist to support you and not the other way around. You’re not in a relationship with your investments so you don’t need to feel guilty about bailing on them, nor should they substitute real happiness. Discipline and pragmatism are key here, and when things don’t go as planned, hoping for the best simply won’t cut it.

Hope isn’t an investment strategy. After evaluating any pros or cons, it might benefit you to take a loss and direct that money and your energy where it has the opportunity to improve.

Choose the right portfolio and diversify your investments

There is a good reason that investment professionals are always talking about diversification — it’s incredibly effective.

When your investments are spread out over a broad range of investment types and vehicles, then losses in one area are likely to be offset by gains in other areas. This has a positive effect on your portfolio and helps manage your emotions too. In turn, a smoother emotional ride helps you control your actions, making it easier for you to stick with your long-term plan.

Choosing a proper asset allocation is important too. This is similar to diversification but specifically refers to your mix of asset classes such as stocks and bonds. Your asset allocation is a major factor in how risky your portfolio is. If your allocation is too aggressive for your risk tolerance, you may end up abandoning it during rough markets.

Your allocation is also important for making sure your investments are aligned with your goals. For example:

- If you need growth and income, you’ll likely have a good mix of stocks and bonds.

- If you are still many years away from retiring and growth is your primary objective, then a portfolio with more stocks is likely a better option.

No single allocation is right for everyone. The best choice depends on the individual investor. Whatever allocation you decide, make sure it fits your risk tolerance and planning goals.

Stay focused on the long term

Patience is a virtue — up and down markets come and go in cycles. Don’t allow yourself to get caught up in the short-term swings or the popular emotional sentiment that surrounds them.

That can be easier said than done though, especially if you aren’t investing correctly. As we have discussed, it’s important to align your investments with your goals and limit your high-risk and volatile investments to an amount of money you can stand to lose in a down market.

That also doesn’t mean you only invest for the long term. Don’t tie up money you’ll need to withdraw soon by purchasing long-term investments with it. If you do and volatility strikes, you’ll be forced to sell and lock in that loss.

Work with a trained professional

For help establishing and executing a plan that supports you, work with a trained professional that has the benefit of experience.

If you’re an investor who’s finding it difficult to keep your emotions out of your investment decision making, then contact Trinity Wealth Management today.

The commentary on this website reflects the personal opinions, viewpoints, and analyses of the Trinity Wealth Management, LLC employees providing such comments, and should not be regarded as a description of advisory services provided by Trinity Wealth Management, LLC or performance returns of any Trinity Wealth Management, LLC Investments client. The views reflected in the commentary are subject to change at any time without notice. Nothing on this website constitutes investment advice, performance data, or any recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Trinity Wealth Management, LLC manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.