If you’re in the market for financial guidance, then you might be looking for an experienced financial professional to help answer your questions and provide advice. But it’s important to know, not all financial professionals are created equal. In fact, you may come across three distinct types: advisors, brokers, and agents.

Each one offers their own benefits and expertise. But who you choose to work with can greatly impact the type of advice you receive and whether they have your best interest in mind.

Here are the differences between each category of financial professionals and how to choose the right one for your financial journey.

Advisor, Broker, Agent – What’s the Difference?

While each of these professionals may appear the same to the general public, there are distinct differences among them, including licensing, compensation, and standard of care.

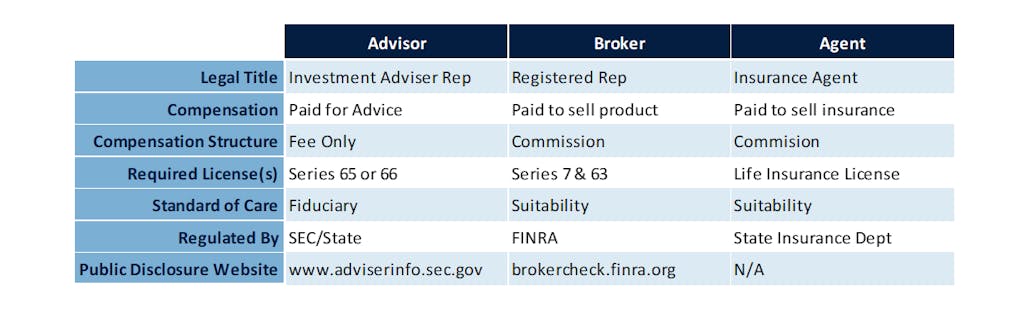

Here’s a quick look at how these financial professionals differ:

Advisors

All three types of financial professionals may use the title “Financial Advisor;” however, only those registered as “Investment Adviser Representatives” are licensed to give financial advice.

These professionals are compensated directly by clients for the advice they give.

While they also can manage investments and make other financial product recommendations, their recommendations are not influenced by how they are compensated. Investment Adviser Representatives do not receive any commissions for selling financial products. Instead, they are fee-only.

This is a key distinction from many other financial professionals because it means advisors do not have a financial incentive to promote certain financial products. Instead, advisors must act as legal fiduciaries at all times and only give advice and recommendations that are in the best interest of their clients.

While this rule seems like it should be an essential and obvious requirement, the reality is many financial professionals who use or adopt the label “Financial Advisor” are not held to this standard. Instead, many are held to a suitability standard, which means the advice and recommendations must only be suitable for you.

To become an Investment Adviser Representative, a person must first pass a Series 65 exam administered by Financial Industry Regulatory Authority (FINRA). This exam tests the advisor’s knowledge of investments, regulations, ethics, and the applicable laws that govern providing financial advice. They are then either regulated by the Securities and Exchange Commission (SEC) or the state in which they operate, depending on the size of the firm for which they work.

You can check an advisor’s registration, experience, and work history on the SEC website.

When an Advisor Might Be Right for You

If you’re looking for conflict-free guidance to help you meet your financial goals, then an Investment Adviser Representative might be right for you. With an advisor, you can rest assured that the recommendations provided have been determined based on your best interest.

Broker

Brokers may also call themselves advisors, but there are big differences between brokers and fee-only advisors.

A broker’s job is to sell financial products for which they receive commissions. For example, when a broker recommends the sale of a financial product to a client, that recommendation is directly tied to the broker’s compensation. This could present an inherent conflict of interest for the broker because their primary goal might be selling certain investment products versus what’s actually best for their clients.

Brokers are not held to a fiduciary standard but instead a “suitability” standard. An investment or financial product can be suitable for your needs but may not be in your best interest. New regulations have attempted to close the gap between suitability and fiduciary standards, but they fall short of making brokers fiduciaries.

Brokers must pass several exams to sell financial products. The most common exam is the Series 7, which allows a broker to sell stocks, bonds, mutual funds, and other securities. In addition, brokers must pass the Series 63 exam, which covers state securities laws.

A broker can also become an Investment Adviser Representative by passing the Series 66 and Series 7 exams. Individuals holding both exam certifications are called dually registered professionals, allowing them to be compensated for advice and for selling financial products.

This can be confusing to clients because the professional may or may not be acting as a fiduciary, depending on which particular service they are providing. A dually registered broker can also sometimes be described as fee-based because they can earn advisory fees in addition to commissions.

You can check a broker’s registration, experience, and work history on FINRA’s BrokerCheck.

When a Broker Might Be Right for You

A broker is a qualified financial professional that can offer financial products that might be right for you. Working with a broker could be beneficial if you are interested in a particular investment vehicle and are not looking for ongoing investment management or advice.

Agent

Agents differ from the other two financial professionals because they focus on insurance products. An agent may work as either a captive agent for a single insurance company or as an independent agent that can offer insurance products from a variety of companies. In either case, their job is to sell insurance, and they are paid commission for making those sales.

Insurance agents must pass a life insurance exam and are regulated by their state’s respective insurance department. While the products they sell must be suitable for their customers, insurance agents are not fiduciaries, and no current website exists to check an insurance agent’s history, like the SEC Advisor Search or BrokerCheck.

Brokers and advisors can also sell insurance products, as long as they have a life insurance license. When a financial professional operates in all three categories, it becomes even more difficult for a client to determine if they are being given fiduciary advice or the recommendation to purchase a product.

When an Agent Might Be Right for You

If you’re in the market for insurance products and are not looking for investment or financial planning advice, then an insurance agent might be the right fit for you. Agents are fully versed in various insurance products and can help you purchase something to fit your goals.

What Else Should I Consider?

In addition to understanding how a financial professional is compensated and the standard of care they must provide, you also want to ensure they have the skills necessary to help you with your financial goals and objectives.

When considering a financial professional, their website is often a good place to start and can help you answer essential questions, such as:

- What do they talk about, and which services do they promote?

- Do they have a clear focus, mission, or investment philosophy, and do you agree?

- Do they have other credentials, such as the CFP® certification? You may wish to search for what these and any other credentials mean to see if they align with your goals.

You’ll also want to interview any advisor you’re considering. Get a feel for their personality and ask them direct questions about how they will communicate with you and how often. Just like in any other relationship, you should view your advisor relationship as more than financial transactions. In the end, you want to choose an advisor you feel comfortable with on both a professional and personal level.

Choose an Advisor Who Works for You

At Trinity Wealth Management, we are all fiduciary financial advisors. We also hold credentials that demonstrate our competence, such as the CFP® certification and Accredited Investment Fiduciary® designation.

We want you to live with financial freedom, and we are ready to help you do just that. Contact us today to learn more about how we can serve your best interests financially.

The commentary on this website reflects the personal opinions, viewpoints, and analyses of the Trinity Wealth Management, LLC employees providing such comments, and should not be regarded as a description of advisory services provided by Trinity Wealth Management, LLC or performance returns of any Trinity Wealth Management, LLC Investments client. The views reflected in the commentary are subject to change at any time without notice. Nothing on this website constitutes investment advice, performance data, or any recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Trinity Wealth Management, LLC manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.