From the gas pumps to the groceries stores, prices on just about everything have been rising drastically.1

In fact, inflation reached a 40-year high2 of 8.6% in June 2022. While increasing costs hurt everyone’s wallets, they can be especially challenging for people on a fixed income, like retirees.

Whether you’re already enjoying your retirement years or close to it, inflation can make it difficult to meet financial obligations now and affect your financial future. Luckily, you can take steps to lessen or mitigate the effects of inflation, so you can enjoy your golden years as planned.

What is inflation?

Inflation measures how quickly prices rise over time. The most commonly used measure of inflation is the Consumer Price Index (CPI), published by the U.S. Bureau of Labor Statistics every month. The CPI tracks price fluctuations in food, clothing, shelter, fuel, transportation, medical services, and other daily costs.

When inflation is high, it reduces purchasing power — meaning it takes more money to buy the same amount of goods and services than before.

While there’s not much we can do to change inflation, there are strategies that can help retirees ease the impacts on their savings.

Here are our top five tips for fighting inflation.

1. Delay major purchases

No one wants to put off a dream vacation or exciting home renovation, but major expenses could cost you substantially more during periods of high inflation.

For instance, since fears of Covid-19 began to ease, travel costs have risen sharply. In June 2022, airline fares jumped 25%3 from year-earlier levels. Hotel prices are also up, with major international cities like New York, São Paulo, and Vancouver posting increases of 60% or more.4 And even the old-fashioned road trip is costlier, thanks to pump prices averaging around $5 per gallon.5

The price of many renovation projects also increased due to rising labor costs and supply chain issues. In 2021, Home Advisor6 found that prices for nearly all types of home renovations rose year over year, with the sharpest hikes in the cost of new cabinets (up 59%), pantries (up 33%), and additions (up 30%).

A major purchase can take a big chunk of your retirement savings when prices are high. If possible, wait until inflation settles down, and you’ll likely see significant savings.

2. Manage expenses

It’s a good idea to evaluate your budget to ensure increased prices aren’t eating into your savings too quickly. Here are some budgeting tips to get you started:

- Look for ways to reduce your costs. Perhaps it’s time to shop around for new car insurance or subscription services.

- Give yourself a monthly limit on entertainment, dining out, and other discretionary spending.

- Cancel any subscription services or memberships you’re not using, or you could do without.

Remember, you don’t need to give up everything. Instead, focus on spending only on what you need or what brings you the most joy.

3. Increase your income

Just because you’re retired doesn’t mean you can’t earn income — and you don’t have to go back to work full-time.

Instead, you may be able to turn one of your hobbies or passions into an income-generating opportunity. Are you a wonderful piano player? Then, maybe you’d like to teach lessons. Do you enjoy painting and drawing? If so, perhaps you can start a successful portrait business. Are you a master typist? In that case, a virtual assistant position may allow you to work from the comfort of home.

If you’re in good health, you might consider a part-time job at a business or organization where you already spend a lot of your time. Alternatively, consider leveraging a lifetime’s worth of skills by offering your expertise as a consultant or independent contractor.

But keep in mind, starting a business — or even taking a job — can affect your social security benefits and taxes. Consider speaking with a tax advisor before getting started.

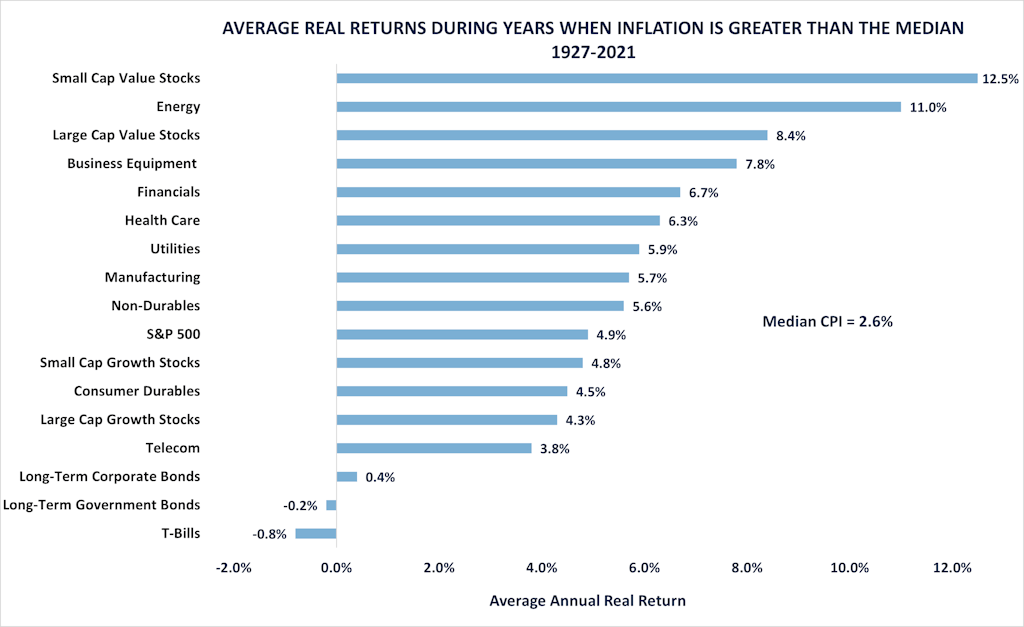

4. Choose inflation-friendly investments

Certain investments perform better in high inflation periods than others, as shown in the chart below.

Sources: Ken French Data Library, Bloomberg. As of 12/31/2021. Past performance is no guarantee of future results. Investing involves risk and possible loss of principal capital. This example is for illustrative purposes and does not represent any actual investment. Returns are average annual total real returns during years when inflation was higher than 2.6% at year-end. Returns are based on results from Kenneth R. French data library using the CRSP database. Universe includes all NYSE, AMEX & NASDAQ stocks. Value represents the lowest 30% of price-to-books (value stocks). Growth represents the highest 30% of price-to-books (Growth stocks). Small and large cap stocks are the smallest 30% of stocks while large cap stocks are the largest 30% of stocks in the universe, respectively. Industries represent the Standard Industrial Classification (SIC) industries for each company.

For instance, while various bonds and cash investments may actually lose value when inflation is high, other sectors like small-cap stocks and energy stocks tend to provide strong returns.

Real assets,7 including real estate, commodities, and precious metals, also typically hold their value as prices rise.

In addition, some investments, like Treasury Inflation-Protected Securities (TIPS), have built-in protection against inflation. TIPS are government bonds that rise and fall with inflation. So, when inflation rises, the interest rate you’re paid increases, too.

Ask your financial advisor to help you review your current portfolio holdings and whether you should make changes to adapt to inflation.

5. Stress-test your plan

It’s one thing to think you’re prepared for higher inflation, but another thing to know for sure. But how can you determine if your savings will hold up to higher costs now or in the future? You can stress-test your portfolio.

Monte Carlo simulation is a complex modeling process that assesses the likely outcomes of a variety of hypothetical scenarios, including high inflation. Stress testing your plan can tell you whether you’re still on track for your goals or if you need to make adjustments.

Your stress test can help you determine whether you might need to adjust post-retirement expenses. It can evaluate the impact of taking social security now versus waiting for higher benefits. Or it can run simulations of how different inflation rates could impact your savings and income.

You can find Monte Carlo simulations on the web, but it can be difficult to interpret the data. Therefore, a financial advisor can provide invaluable insight into stress-test results.

Managing inflation takes planning

These five strategies can help you adapt to a higher inflation economy and ensure your retirement goals stay on track.

If you’d like to learn more about inflation-proofing your retirement, then contact us today to schedule a consultation with our retirement planning specialists.

The commentary on this website reflects the personal opinions, viewpoints, and analyses of the Trinity Wealth Management, LLC employees providing such comments, and should not be regarded as a description of advisory services provided by Trinity Wealth Management, LLC or performance returns of any Trinity Wealth Management, LLC Investments client. The views reflected in the commentary are subject to change at any time without notice. Nothing on this website constitutes investment advice, performance data, or any recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Trinity Wealth Management, LLC manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

Sources:

1 “May inflation breakdown: Where are prices rising the fastest?” Fox Business

2 “U.S. inflation hit a new 40-year high last month of 8.6 percent,” Politico

3 “Airline ticket prices are up 25%, outpacing inflation — here are the ways you can still save,” CNBC

4 “This Summer’s Hotel Rates Will Keep You Up at Night,” Bloomberg

5 “Today’s AAA National Average,” AAA

6 “True Cost Report 2021,” HomeAdvisor

7 “3 Best Investments for Inflation,” U.S. News & World Report