Few retirement decisions are as nuanced as when to claim Social Security. What’s right for your neighbor, your sibling, or your coworker may not be right for you. The age at which you claim affects your benefit for the rest of your life, and the right answer depends on your health, your other income sources, your spouse’s situation, and how you think about risk.

There’s no single “correct” age to claim, but there is a right process for thinking it through, and that’s what we’ll walk through here.

How Social Security Timing Works

Your Social Security benefit is calculated based on your 35 highest-earning years, and the amount you receive each month depends on both your earnings history and when you begin collecting.

The Social Security Administration (SSA) assigns everyone a Full Retirement Age (FRA), which is the age at which you’re entitled to your full, unreduced benefit. For anyone born in 1960 or later, FRA is 67. If you were born between 1955 and 1959, your FRA falls somewhere between 66 and 2 months and 66 and 10 months. The SSA’s website has a quick lookup tool if you’re in that window.

From there, the rules work in both directions:

- Claim early, as young as 62, and your benefit is permanently reduced by up to 30% for someone whose FRA is 67.

- Claim late, up to age 70, and your benefit grows by 8% per year of delay past FRA, for a maximum increase of 24% (again, for those with an FRA of 67).

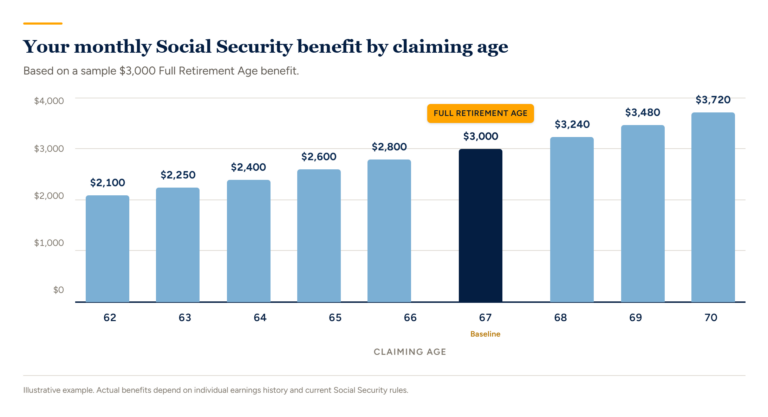

To put that in perspective, here’s how a hypothetical $3,000-per-month FRA benefit changes based on when you claim:

Example is hypothetical and for illustrative purposes only. Actual benefits will vary based on individual earnings history.

In the hypothetical example above, the benefit is reduced to $2,100 if claimed early at 62, and increased to $3,720 if delayed until 70. That’s a significant range, but it’s only half the picture. Claiming earlier means more total checks; claiming later means larger ones. Which adds up to more lifetime income depends on how long you live, which is the one variable no one can know in advance.

Factors That Point Toward Claiming Earlier

There are genuine situations when claiming early makes sense. It means having the money in hand sooner, which is its own kind of certainty in a decision with so many unknowns.

Your health or family history is a real concern. If you have reason to believe your life expectancy is shorter than average, based on your medical history, family longevity patterns, or a current diagnosis, claiming earlier may make sense.

You need the income. If your savings or other income sources aren’t enough to cover your expenses like health insurance before Medicare at 65, claiming Social Security may be the most practical choice. It can be better to claim early on your own terms than to be forced into portfolio withdrawals at an inopportune time.

You’d rather start using the income now. Money in your 60s often funds the most active years of retirement. For some, having income they can count on today matters more than the chance of a higher Social Security benefit later.

You’re no longer working. If you plan to stop working before your FRA, the reduction for claiming early is straightforward. If you’re still working and claim before your FRA, be aware of the Retirement Earnings Test. Social Security can temporarily withhold a portion of your benefits if your earned income exceeds a certain threshold. Those withheld benefits aren’t lost forever (they’re recalculated into a higher benefit at your FRA), but the test can complicate the cash flow picture in the meantime.

A note on spousal benefits and timing. It’s a common misconception that a lower-earning spouse can simply claim early “while the higher earner delays” without consequence. In reality, if the lower earner claims a spousal benefit before reaching their own FRA, that spousal benefit is permanently reduced, even if the higher earner waits. The maximum 50% spousal benefit is only available if the lower earner waits until their own FRA. That doesn’t mean early claiming is wrong for the lower earner. If other circumstances make it the right call, the tradeoff is just worth understanding before filing.

Factors That Point Toward Waiting

There are also genuine situations when waiting makes sense.

You’re in good health with a family history of longevity. If you have reason to expect a long retirement based on family longevity and current health, delayed claiming may produce more total lifetime income, though it depends on how the years actually play out.

You have other assets to draw from in your 60s. If you can fund early retirement spending from your savings, you have the option to delay Social Security. Drawing on your savings in those years lets your future Social Security benefit increase.

You’re the higher earner in a married couple. The surviving spouse receives the higher of the two benefits, so the timing decision made by the higher earner directly affects what the surviving spouse will receive, potentially for decades. It’s one reason couples benefit from coordinating both claiming decisions.

Tax planning. Drawing from your retirement accounts in the years before claiming Social Security can lower your future Required Minimum Distributions, easing potential tax exposure later. It also creates room for Roth conversions during those years, which work best when Social Security income isn’t already adding to your taxable income.

Consult a tax advisor before making decisions based on tax planning strategies discussed here. Tax outcomes vary by individual situation.

Understanding the Break-Even Point

When researching Social Security timing, people often land on the concept of a “break-even age”: the point at which the cumulative benefit from claiming later overtakes the cumulative benefit from claiming earlier. For someone with an FRA of 67, that crossover typically falls in the late 70s to early 80s, depending on the assumptions used.

The catch is that you only really know in hindsight. If you live past break-even, waiting will have paid off. If you don’t, claiming earlier will have. And in many cases, spousal benefits, taxes, and your overall income plan are bigger considerations than break-even itself.

Break-even estimates are illustrative and depend on assumptions including benefit amounts, inflation, and investment returns. Individual results will vary.

A Few Things Worth Knowing Before You Decide

Early claims aren’t easily undone. If you claim before FRA and change your mind, you have a 12-month window to withdraw your application, but you’ll need to repay everything Social Security has paid you. After that window closes, your options narrow considerably.

COLAs apply whether you’ve claimed or not. Your benefit base receives annual cost-of-living adjustments starting at age 62, so your benefit grow over time regardless of when you actually file.

Don’t confuse Social Security and Medicare timing. Medicare starts at 65, regardless of when you claim Social Security. If you’re collecting Social Security by then, your Part B premiums come out of your check automatically; if you’ve delayed, you’ll pay them separately.

The Takeaway

There’s no universal right answer on Social Security timing, but there is a right way to think about it. The decision should be grounded in your health, your other assets, your household income strategy, and a realistic view of your retirement timeline.

If you’d like to talk through how this applies to your situation, our team is happy to help. Contact us to get started.

This content is intended for informational purposes only and should not be construed as personalized financial, tax, or legal advice. Please consult with a qualified professional regarding your specific circumstances.

The Bottom Line

Beneficiary designations are easy to overlook, but they’re a foundational part of any estate plan. They control where some of your largest assets go, they bypass your will, and once you’re gone, mistakes can’t be corrected.

The good news is that reviewing them is one of the simpler things you can do for your estate plan. If you’d like a second set of eyes on your estate plan, or want to make sure your designations align with the rest of your goals, reach out to our team and we’ll walk through them with you.

The commentary on this website reflects the personal opinions, viewpoints, and analyses of the Trinity Wealth Management, LLC employees providing such comments, and should not be regarded as a description of advisory services provided by Trinity Wealth Management, LLC or performance returns of any Trinity Wealth Management, LLC Investments client. The views reflected in the commentary are subject to change at any time without notice. Nothing on this website constitutes investment advice, performance data, or any recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Trinity Wealth Management, LLC manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.